{kind=link}

{kind=link}

{kind=link}

How is my Dental Coverage?

We get this question all the time. We treatment plan for patients at their first appointment providing them with exactly what is their portion to pay and what their insurance covers. This question is typically prompted when a patient has an HMO plan or they thought their PPO had higher coverage. We understand that picking the right insurance is hard and when you are talking to an insurance agent about the “best plan” they may make it seem like it really is the most magical dental coverage out there (when they are just doing their job to sell the plans). Now, we are not saying your dental coverage is bad, but we want to make sure everyone understands what other options are out there. We really care about our patients here at the Dental Health Center so we wanted to dive deeper into educating our patients on what dental insurance plans are and what they are really covering.

PPO Plans:

The PPO plan is a specific type of plan tied to a network of dentists who sign a contract with the insurance company in agreement to a specific fee schedule and follow a set of rules and guidelines. This plan allows reimbursement for both in and out-of-network providers. There will typically be some sort of deductible along with a yearly annual maximum the insurance will pay per year.

The common PPO plan includes a $50 deductible, an annual maximum of $1000.00, basic insurance coverage at 80%, major insurance coverage at 50%, and no implant coverage.

If you see an out-of-network provider, you do have to be careful and make sure your PPO plan has an out of network benefit to ensure reimbursement for your visit. While you can be seen at an out-of-network provider, some providers may require you to act as an out-of-pocket patient where you pay upfront and submit the claim yourself for reimbursement. It is all situational based per office.

The Dental Health Center only deals with in-network plans to avoid any confusion or hassle for the patient. We also submit all claims. If we happen to be out of network for your insurance company, we will get credentialed and move forward as usual.

Most major insurance companies offer a PPO plan like Delta Dental, Cigna, Aetna, United Concordia, and MetLife.

HMO/DHMO Plans:

HMO and DHMO are interchangeable terms. It can also be known as a CAPITATION Plan. These plans will only provide reimbursement for services through an in-network provider. These plans typically require some sort of copay and do not usually have deductibles or annual maximums.

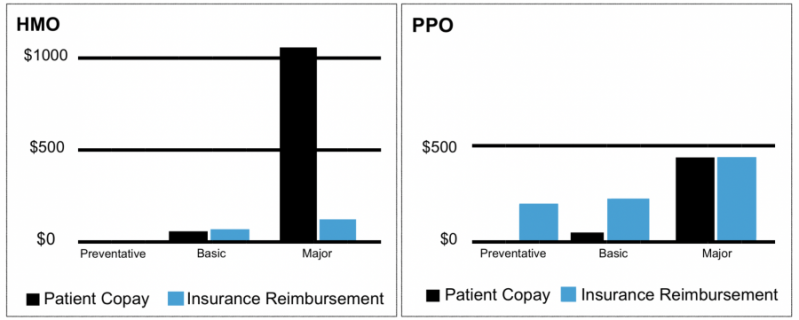

HMO plans are offered by most of the same major dental insurance companies as the PPO plans. HMO plans typically have much lower to free premiums for employers and members which is what makes them so attractive. Often times people are misled with the HMO plan advertising a low premium and good coverage without acknowledging it is mostly a Copay plan which, in result, could be a bigger out of pocket expense in the long run rather than a PPO plan itself with a higher premium (see graph below).

Most HMO plans (specifically Cigna) advertise that they pay a remaining percentage after you pay your Copay. Now, this may be correct in some cases, but in most cases, it is a misconception. The insurance company has an agreed fee for a procedure code. If the agreed fee is higher than the Copay, they will pay the difference. However, in my experience, many of the Copays are higher than the agreed fee. In result, the only payment we are getting for the procedure is the Copay.

Capitation plans pay a fixed amount to the dental office each month for each enrolled person assigned to the dental provider. In exchange for the monthly payment, the provider agrees to do some procedures for free (typically, diagnostic, preventative, and fillings) and others for a very reduced fee. This is why you have a hard time finding a dental office that takes HMO plans.

***For ALL dental plans, dental services that are not covered by the plan must be paid by the patient at the dental offices full fee.

When looking for the best coverage you want to think about the following items:

- A maximum higher than $1000 per year.

- A deductible lower or equal to $50.

- Basic coverage of 80% or more (this is your fillings, periodontics and sometimes endodontics and oral surgery).

- Major coverage of 60% or more (this is your crowns, prosthetics and sometimes endodontics and oral surgery).

- No missing tooth clause.

- No waiting periods.

- Implant/Crown coverage.

- Making sure it is not a coverage increasing plan per year of contract.

Note: There are some coverages out there that have 100% coverage for any procedure (except cosmetic) up to the annual maximum amount. I am not sure how much the premium is for this kind of plan, but I have seen those dental coverages through Humana and Cigna.

Insurance Plans we Recommend:

Cigna Dental Indemnity

Humana Medicare Dental POSD

United Concordia PPO/PFT/Keystone 65+

Cigna PPO

Physicians Mutual

United Health Care Dual Complete Medicare

Delta Dental PPO (depending on coverage percentages)

For a list of dental insurances we take, please click here.

Ready to Schedule a Consultation?

Dr. Shock offers a number of dental treatments that can keep your mouth healthy and your smile beautiful. Contact us today!